扫一扫又不会怀孕,扫一扫,作业无烦恼。

留学顾问の QQ:2128789860

留学顾问の微信:risepaper

转眼间已经进入2021年份的最后一个月,今年总结起来就是变幻动荡的一年,也是业务暴增的一年,实现了很多心中埋藏许久的小目标,相信明年的业务量会更多,会需要更多的经历来处理代写订单。人生就是这样,向上的道路会越来越难走。饭一口一口吃,自己加油!

- 在第五题的答案中,我们应该注意On default, we assume that the loss is 1R, where R is a xed recovery of par/notational. If t = , then we write the time to default in terms of the inverse cumulative distribution

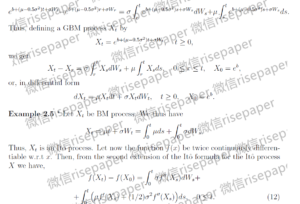

- Express the joint density function of W2;W4;W6 in terms of the transition density function

of (Wt; t 0): - Topic 2b): (One-dimensional) Brownian Motion Process Compute the probability density function of W4 conditional on W2 = 0 and W6 = 0:

- Topic 3): Stochastic Integration, It^o Formula, Stochastic Dierential Equations, and Girsanov Transformation代写

- Thus, process M is martingale with respect to the natural ltration of N (cf. Exercise

4 below). This is the result that you already know (cf. Topic 2a), Remark 3.7. - To get some practice, you may start from verifying the martingale property for s = 0; that is,

verifying that for any t 0 we have that - Determine the long run probability that a failure occurs in a given period. Determine the long

run probability that the component operating in any time period is two units of time old. - The lifetimes of consecutive components are independently distributed. Thus, the process X dened as:

Xn = the age of the component in service at time n

is a Markov chain. By convention, we set Xn = 0 at the time of failure. - The long run probability that a failure occurs in a given period is (0) = 10=23: The long run

probability that the component operating in any time period is two units of time old is (2) = 4=23: - Let Xn; n = 0; 1; 2; : : : ; be a time homogeneous Markov chain dened on the probability

space (

;F;P) and taking values in the nite state space S. Verify that for any k = 1; 2; : : : ; and any

i; j; ` 2 S it holds that