扫一扫又不会怀孕,扫一扫,作业无烦恼。

书来了,The recommended textbook for this module is

Hall, J. C. (2016) Fundamentals of Futures and Options

Markets, 9th Edition, Pearson.

The forward price for a contract is the delivery price that would be

applicable to the contract if negotiated today (i.e., it is the delivery price that

would make the contract worth exactly zero).

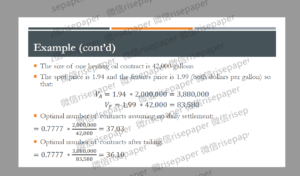

The forwards price may be different for contracts of different maturities (as

shown by the table in the next slide).

第一题C问的要求是,Calculate the prices of Treasury bonds with 5, 15, and 25 years until maturity. In each case, assume the face value of $100 and the coupon rate of 6% per annum and that coupons are paid quarterly. Assume quarterly compounding. In case your interest rates dataset does not include a required maturity, apply an average of the rates corresponding to the closest maturities. Discuss the results.

分析五种情形,How would your results obtained in a) change in each of the following four cases (consider each of the points below separately)? Explain.

a. Quarterly compounding

b. Annual compounding

c. Simple compounding

d. Coupons being paid out semi-annually

e. Coupons being paid out annually

应当认真参照评分要求去excel分析数据集并认真写原创的report. Prepare your dataset of the daily stock prices, risk-free interest rates, and the six-month futures prices to cover all the calendar days during the analysed period.