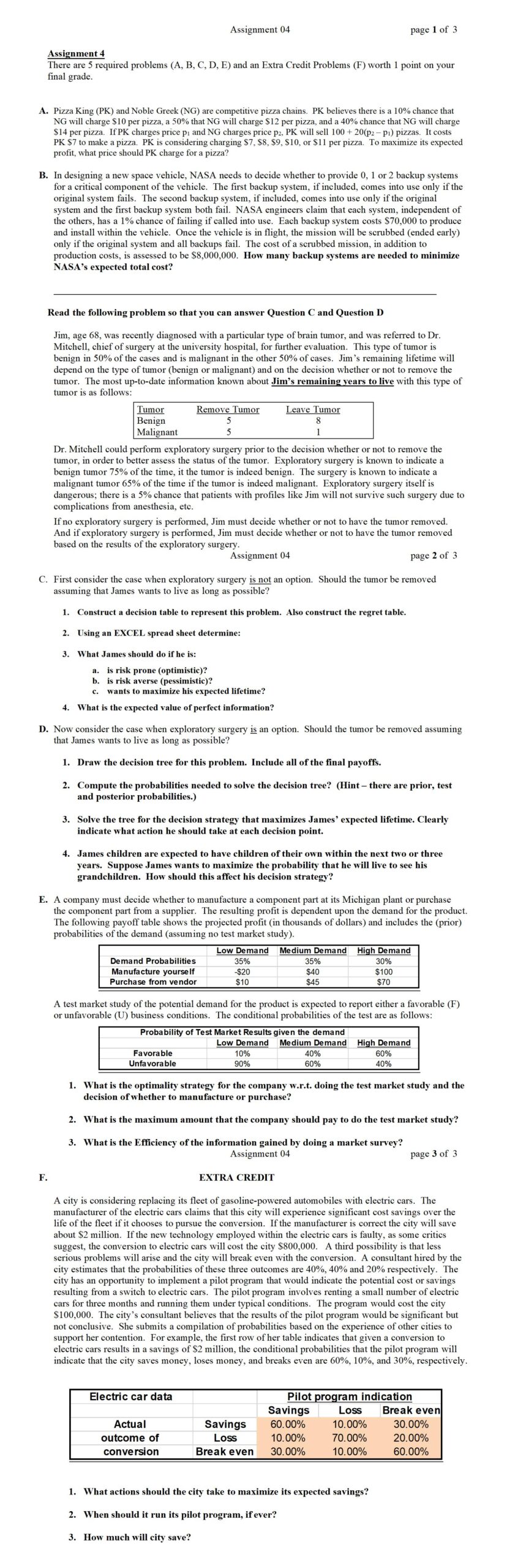

留学顾问の QQ:2128789860

留学顾问の微信:risepaper

注意

每道题目做完以后

把excel spread sheet 截屏以后,复制粘贴到word里面

锐泽代写,专注于留学生在线解压,在线online课业烦恼不要犯难,一站式解决方案

Assignment 5

(This assignment is based on Problem 13.23 (edition 4) which you can find at the bottom. Do not do 13.23)

Jennifer was just born and her parents have decided to save money to pay for her college education. They will invest $15,000 right now, and $10,000 each year on her future birthdays for the next 17 years (i.e. $10,000 when she turns 1, 2, 3, … 16, 17). They are bullish on America and are investing all of this money in the stock market. The principal and returns are allowed to accumulate (i.e. are reinvested) in the equities market and no distribution of funds will be done before Jennifer starts college. Assume that the returns of the stock market are normally distributed and are independent from year to year with a mean (µ) return of 7% and a standard deviation (σ) of 10%. All investments returns are tax free.

REQUIRED – Jennifer is planning to go to college starting on her 18th birthday; hence it is important for the parents to know how much money will have accumulated in her College Fund at that time (Call this the ACCUMULATION of the College Fund). Construct a Monte-Carlo simulation model in EXCEL or CRYSTAL BALL (EXCEL add-on) to model the problem. Run the simulation for at least 1,000 trials to answer the following questions:

- What is the mean and the standard deviation of the ACCUMULATION?

- What is the probability that the ACCUMULATION is over $300,000? over $350,000? over $400,000?

- What is the ACCUMULATION if the standard deviations is zero. (Fixed return)

- Can you compute a 95% confidence interval estimate of ACCUMULATION? If so, what is it? If not, why not?

- Can this problem be solved without using simulation? If so, how?

EXTRA CREDIT – Now consider the case where the rates of return are not independent from year to year. There is an idea in finance that if returns are higher in a given year they will be lower in the next year. (MEAN REVERSION). Assume the following model:

The mean return in a given year = 7% – α (Last year’s return –7%)

- Modify your initial model and answer questions “a”, “b”, and “c” for α = 0.25, 0.5, and 1.0

- How do the results of this model compare with the original model? Are they what you might have expected? Comment.